Performing vs Non-Performing Notes: Key Differences Every Note Seller Must Understand

If you own a business note or mortgage note, understanding performing vs non-performing notes is critical—especially if you’re considering selling it. These classifications directly impact the value of your note, the type of buyer it attracts, and how quickly you can convert it into cash.

In this article, we break down what performing and non-performing notes are, how they differ, and what note sellers need to know before entering the secondary market.

What Are Performing Notes?

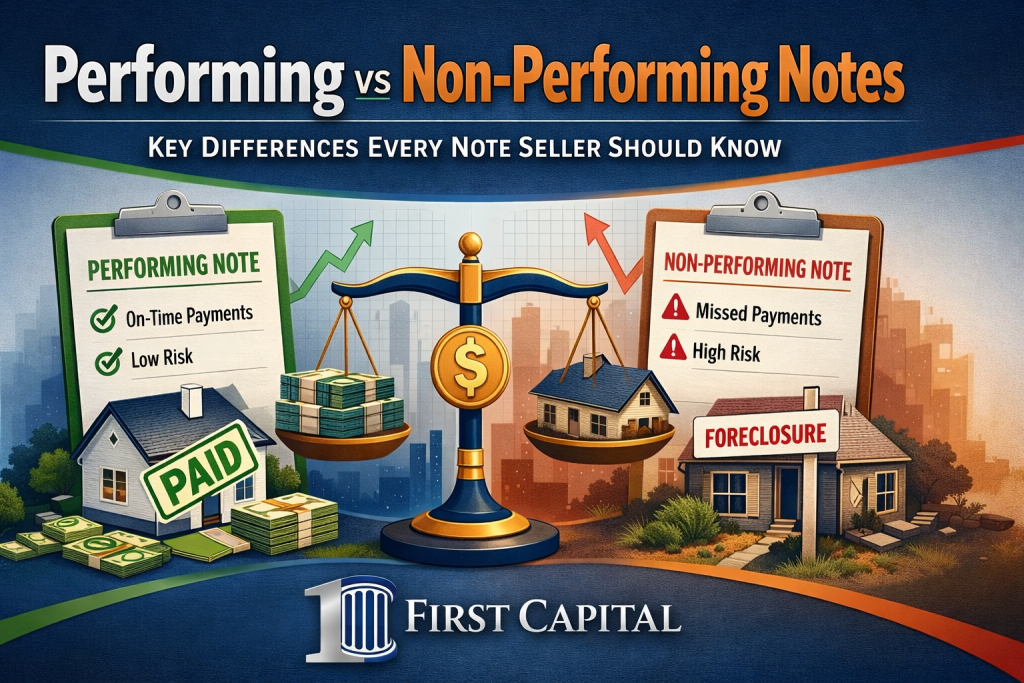

A performing note is a loan where the borrower is making payments on time and according to the agreed-upon terms.

Key Characteristics of Performing Notes:

- Payments are current (typically no more than 30 days late)

- Consistent payment history

- Lower risk for investors

- Predictable cash flow

These notes are considered income-producing assets. Because of their reliability, they are highly attractive to note buyers and typically sell at higher prices—often closer to their unpaid principal balance.

Examples of Performing Notes:

- A mortgage where the homeowner pays monthly without delay

- A business loan with consistent repayment history

- Seller-financed real estate with a strong borrower track record

What Are Non-Performing Notes?

A non-performing note (NPN) is a loan where the borrower has stopped making payments or is significantly behind—typically 90+ days delinquent.

Key Characteristics of Non-Performing Notes:

- Payments are late or completely missed

- High risk of default

- Irregular or no cash flow

- May require legal action or restructuring

Non-performing notes are often viewed as distressed assets. While they carry more risk, they can still be valuable—especially to experienced investors who specialize in workouts, restructuring, or foreclosure strategies.

Examples of Non-Performing Notes:

- A mortgage in foreclosure

- A borrower who hasn’t paid in several months

- A business loan in default

Performing vs Non-Performing Notes: Key Differences

Understanding the distinctions between these two types of notes is essential if you’re evaluating a sale.

1. Cash Flow Stability

- Performing Notes: Reliable, predictable income

- Non-Performing Notes: Little to no current income

2. Risk Level

- Performing Notes: Low risk

- Non-Performing Notes: High risk

3. Market Value

- Performing Notes: Sell at a premium (higher percentage of balance)

- Non-Performing Notes: Sold at a discount due to uncertainty

4. Buyer Type

- Performing Notes: Passive investors seeking steady returns

- Non-Performing Notes: Active investors skilled in asset recovery

5. Exit Strategy

- Performing Notes: Hold for yield or sell for lump sum

- Non-Performing Notes: Modify loan, foreclose, or liquidate collateral

Which Type of Note Is Easier to Sell?

Performing notes are generally easier to sell because they offer immediate income and lower risk. However, non-performing notes can still attract strong interest—especially if:

- There is valuable collateral behind the note

- The borrower has potential to re-perform

- The note is secured by real estate

The key is working with a buyer who understands how to properly evaluate and price both types of assets.

How Note Value Is Determined

Whether your note is performing or non-performing, buyers will evaluate:

- Payment history

- Remaining balance

- Interest rate

- Collateral quality

- Borrower creditworthiness

- Time remaining on the note

Performing notes typically receive higher offers, while non-performing notes are priced based on risk and recovery potential.

Should You Sell Your Note Now?

If you’re holding a note—performing or not—you may be sitting on a valuable asset that can be converted into immediate cash. Many note holders choose to sell in order to:

- Eliminate risk

- Improve cash flow

- Reinvest capital

- Avoid dealing with delinquent borrowers

Sell Your Notes with First Capital

At First Capital, we specialize in purchasing both performing and non-performing business notes and mortgage notes in most states nationwide.

Whether your note is generating steady income or facing challenges, our team can provide a fast, fair evaluation and a no-obligation quote.

Why Work with First Capital?

- Competitive pricing

- Fast closings

- Simple, transparent process

- Expertise in both performing and distressed notes

Get a Free Note Evaluation Today

If you have questions about your note—or you’re ready to sell—contact First Capital today. Our team is here to help you understand your options and maximize the value of your asset.

Reach out now to get a no-obligation mortgage note quote or a no obligation business note quote and turn your note into cash.